Even if one assumes there is relatively-constant pressure on retail communications service products, those price trends for fixed and mobile network services need deciphering.

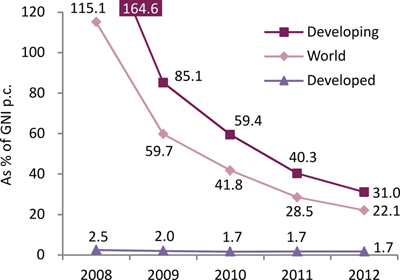

Global prices, measured as a percentage of gross national per-capita income, have fallen at least since 2008, according to the International Telecommunications Union. But what requires explanation is higher prices, where they happen.

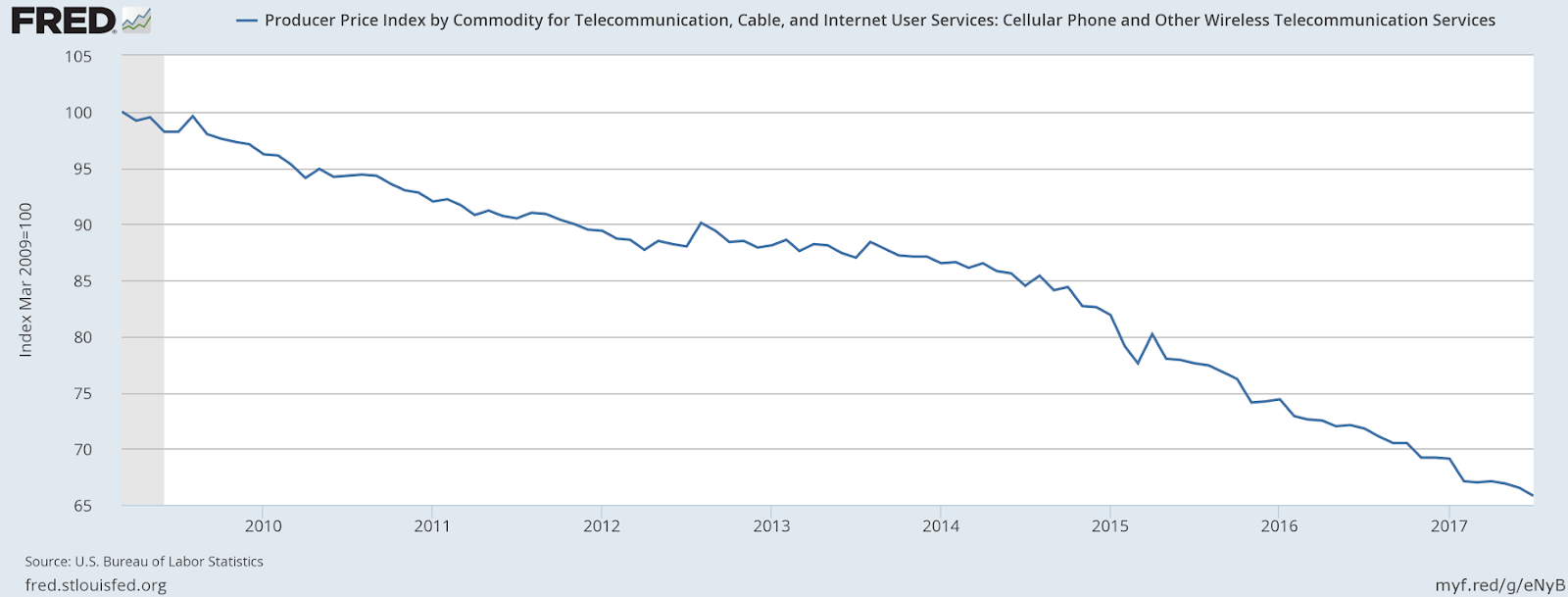

In the U.S. market, since at least 2009, prices have generally fallen for some products such as mobile service, mobile voice and texting.

Also, internet access prices have fallen about five percent since 2009. But prices for fixed network voice and content subscriptions have risen.

Even prices for internet access services, generally stronger in some quarters because consumers now are buying faster services that cost more than slower services, have dipped since 2009, with most of the drop happening in 2017.

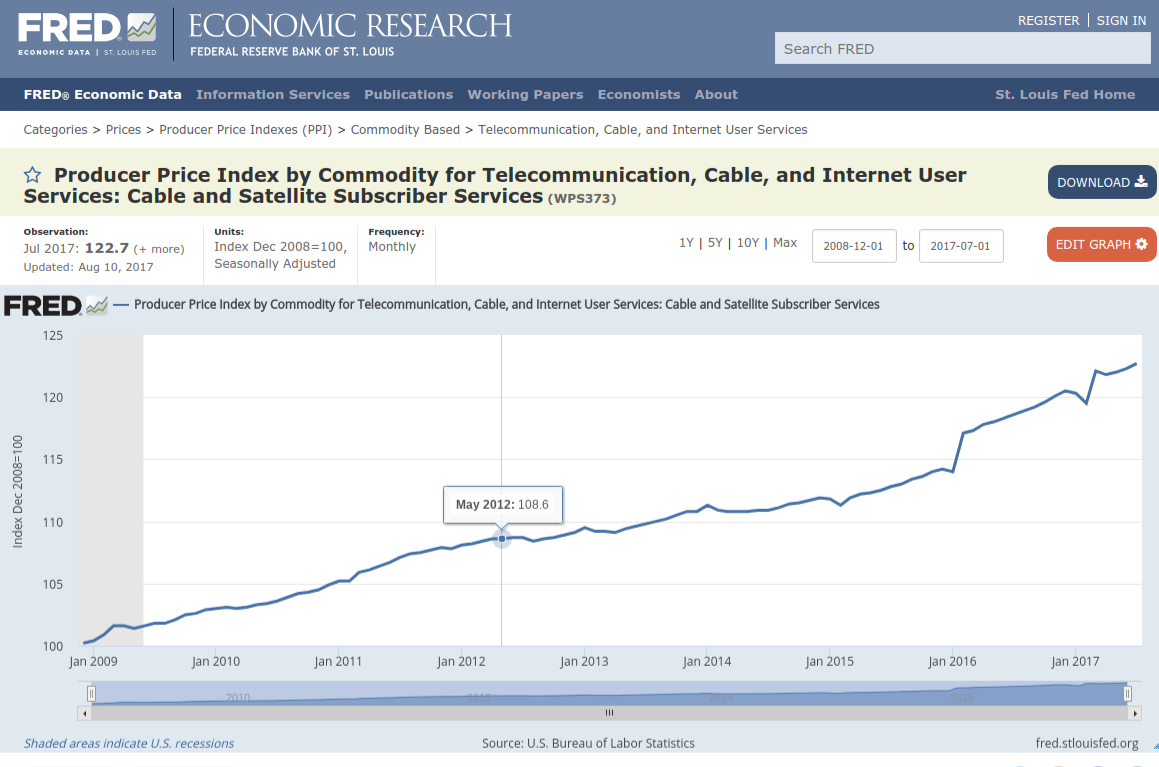

The exception to the trend of falling prices are subscription TV services, which have seen growing prices since 2009. So what makes content services different from internet access and mobility? Internet access is the classic “dumb pipe” service, hard to differentiate and subject to Moore’s Law fundamental trends (constantly increasing quantity, constantly dropped price per unit).

Subscription TV is a content service, more analogous to websites, music and fashion than a “telecom” service. Also, the value of mobility these days is arguably more weighted to internet-accessed apps and content than to carrier voice and messaging functions. That is to say, more of the value of a mobile service now is the dumb pipe access to content and apps, and less the carrier voice and messaging services.

Ironically, one might also note that prices for fixed network voice service, a product far fewer consumers now buy, have grown since 1996, when local telecommunications was deregulated in the U.S. market. Since about 1996, prices have climbed about 35 percent. There are a couple reasons, amongst them the ability of suppliers to raise prices more easily, despite the countervailing trends of declining demand and greater competition.

The other issues are likely that the mix of business and consumer lines has been changing, with a greater percentage of business lines, compared to consumer lines, than has been the case in the past. Also, consumers who do not value fixed network voice services already have deserted for mobile services. The consumers who remain likely place a higher value on fixed network voice.

On the whole, basic economic principles seem to be at work. Generally speaking, demand for any product will grow with lower prices and fall with higher prices. Higher prices for fixed network voice have definitely been accompanied by lower take rates.

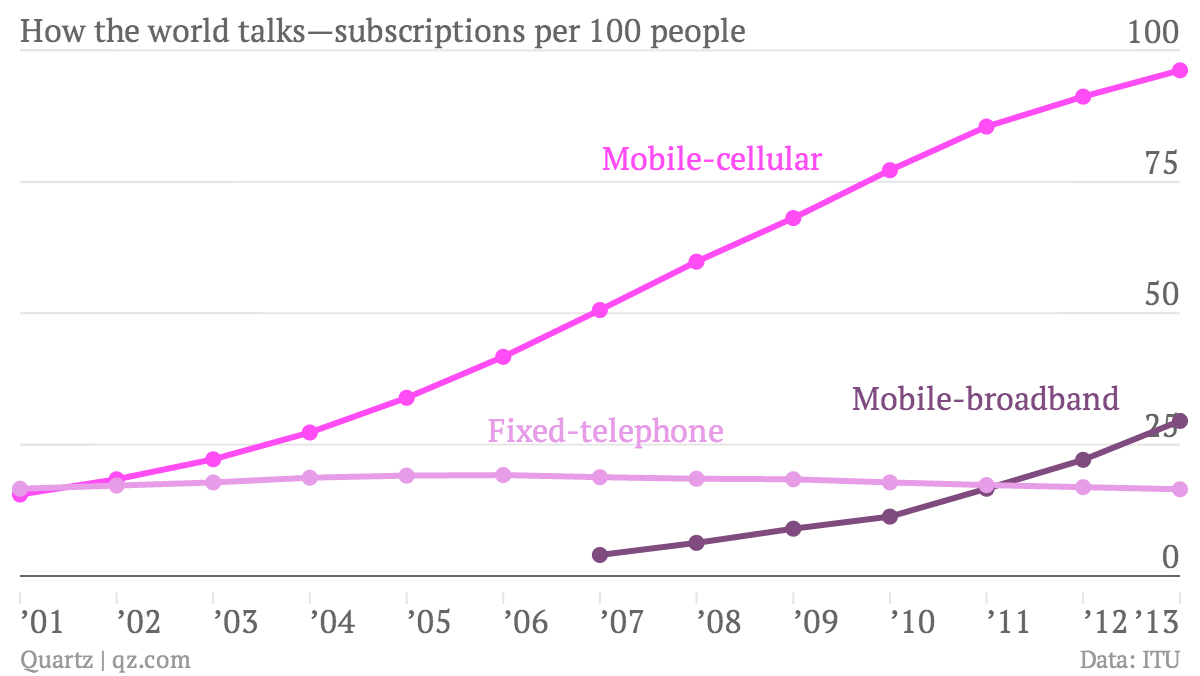

Globally, fixed telephone accounts seem to have peaked about 2006.